| TGS insights give you the stories behind Energy data. These regular short 3-5 minute reads feature thought provoking content to illustrate the use of Energy data in providing insight, nurturing innovation and achieving success. |

Introduction

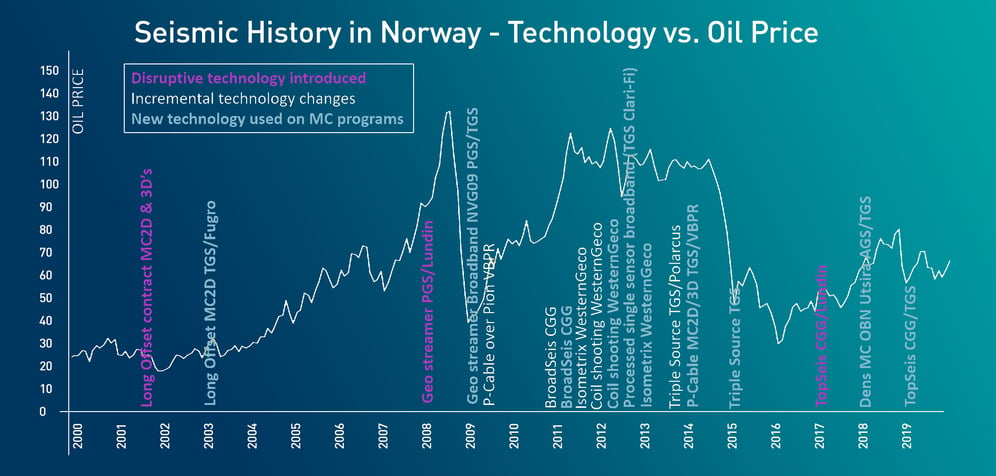

Both incremental and disruptive advances in the development of seismic imaging technology have been crucial for regional geological mapping as well as oil and gas prospect definition. While revolutions in offset, broadband, azimuthal and density implementation have been crucial in streamer seismic development over the last 15-20 years, the next generation of seismic is likely to be shaped by OBN, with steadily increasing amounts of sources and new advances in processing.

2D and 3D Developments

Most recently, the waters in northern Europe and the northern Gulf of Mexico have been two highly active testing grounds for new technological advances. In the Norwegian part of the North Sea we have experienced the third generation of seismic 3D acquisition; nearly all mature areas have two generations of streamer 3D.. Additionally, seismic data processing technology has seen a similarly steep learning curve as hardware capabilities and disk space have increased. These days, new processing technology steps are occurring in the cloud, where computing power and disk space can be expanded as needed.

Before 2000, the North Sea database generally consisting of seismic with 3 km streamer lengths. The offset revolution occurred around the start of the millennium when a few 2D and 3D surveys using 5-6 km streamers began to appear. The new prevailing standard was cemented when TGS and Fugro acquired their North Sea Renaissance multi-year 2D program using 6 km offsets for 3D and 8 km for 2D. Since that time, “long offset” became a buzzword in the industry, and all vessel owners bought more streamer sections to remain competitive.

A Chart plotting the historical oil price against significant technological developments in seismic acquisition

Since the dawn of 3D acquisition in the 1980s, almost all improvements have happened on the streamer side. Dual source-based air-gun arrays became a standard and, besides some alterations of output volume and frequency of the outgoing signal, little else happened. Today, triple source has become the new standard, and many deblending approaches exist and are continuously being improved. The source battle is still ongoing, and configurations of five or six sources have been used in production. Up to ten sources are now a future prospect.

Ocean Bottom Node (OBN) Technology

Lying almost dormant for 30 years since the first tests in the NCS, due to the historically high acquisition cost, is Ocean Bottom Node (OBN) full azimuth technology. This seismic technology can outperform streamer seismic in nearly all quality aspects, except for very shallow targets. New approaches in deployment and the use of triple source vessels has made large scale dense OBN possible, such as the Utsira OBN in the North Sea acquired by TGS and AGS.

By using OBN, challenging complex targets like sand injectites are now illuminated from all sides and sampled up to 25 times better than with a narrow azimuth streamer 3D. The natural continuous recording of OBNs combined with deblending allows extraction of extremely long records in processing, both in time and offset. This has been tested on Utsira OBN data extracting node gathers with maximum offsets of 20 km, and the resultant gathers have been used as the input for model building based on diving wave Full-Waveform Inversion (FWI). The latter was motivated by the recent successes in subsalt inversion and imaging with Sparse OBN surveys in the Gulf of Mexico, where advanced model building with ultra-long offset FWI has been leveraged. The future direction of the energy industry is always hard to predict. Still, surely OBN, with steadily increasing amounts of sources and new advances in processing, will together play an increasing role in North Sea exploration activities.

.

The OBN Utsira dense nodal (300 x 50m) project just west of the Johan Sverdrup field, for example, has recently been delivered and portions of the data have already been utilized for de-risking oil and gas prospects. In addition, several reprocessing projects targeting specific fields or prospects are ongoing within operator’s offices and at TGS. This is a clear indication that OBN will be reprocessed again and again at least for the next decade. Historically, the big hurdle has always been the acquisition cost. However, with the combination of multi-client projects, new deployment techniques, and the utilization of multiple semi-simultaneous sources, the cost for a typical production license has made large scale OBN more accessible. Still, cost is just one of the challenges presented by OBN, another one is data volume and turnaround time. The OBN Utsira project is the world’s largest when it comes to recorded data weight which resulted in new ways of thinking from TGS in terms of processing, transport, and storing facilities.

Driving Forward

The seismic industry has seen both incremental and disruptive technology changes during the past 15 years. All players need to strive to be involved in driving technology forward, not just in terms of acquisition but also imaging technology and data insight, in all areas of the energy sector. However, the focus remains on economy of scale and long-term value.

This TGS insight is based on an article which appeared in issue 7, 2020 of Geo Magasin written by Bent Kjølhamar, Adriana Citlali Ramirez and Sindre Jansen (TGS). To see the full version of this article CLICK HERE.