| TGS insights give you the stories behind Energy data. These regular short 3-5 minute reads feature thought-provoking content to illustrate the use of energy data in providing insight, nurturing innovation, and achieving success. |

Some experts have argued that a rapid transition to renewables and complete removal of hydrocarbon exploration could lead to the collapse of technological progress and medical advancements as we know them. Natural gas exploration promotes the exploration and derivation of elemental gases like hydrogen, nitrogen, and helium, without which modern technology would not be possible. Helium, in particular, is necessary for everything from space exploration and medical imaging to cloud computing and scanning your groceries.

Although helium is the 2nd most abundant element in the universe, it is a rare commodity on earth. Recent global events have restricted supply while continued technological growth is expanding demand, causing a sharp rise in the price of helium and spurring a new drive for exploration and production of new sources.

|

Join the ConversationAt TGS we create unique, actionable insights from raw energy data. These insights can reduce risks and enable a more detailed understanding of natural resource investments. Follow us to #SeeTheEnergy and JOIN THE CONVERSATION >> |

THE IMPORTANCE OF HELIUM

Helium is an inert, non-flammable, colorless, odorless, and tasteless gas with the lowest boiling point of any element at -268.93º c (-452.07º f). Due to this low boiling point, helium provides an ideal environment for advanced electronic hardware to operate.

Helium is also unique as it has properties that no other known element can replicate. The possibility for quantum computing, nuclear fusion, and more efficient space travel are not attainable without helium, not to mention current uses in semiconductors, computer memory, fiber optics, and the medical industry.

HELIUM SHORTAGE

The US government was the biggest supplier of helium for decades, providing 40% of the supply from its BLM (Bureau of Land Management) storage facility in Texas Panhandle until 1996, when the Helium Privatization Act deflated prices. As the technology sector grew in the 2000s, a growing demand saw reserves severely depleted, and a series of helium shortages became apparent. This led to a new law in 2013 forcing the US government to auction helium at market value, providing private investors an incentive to build new plants and seek new sources. The final US sale of its helium interests will be completed in September of 2022, allowing the commodity to be driven by free-market principles.

The last two decades have seen slow progress in the development of new sources and processing facilities. Many countries and investors are playing a game of catch-up to mitigate the damage from dwindling supply. The global shutdown induced by the COVID pandemic further hampered supply and had wide-ranging implications for demand.

The supply issues already affected by recent global shortages have been compounded by political instability and production setbacks at a number of locations. For example, fire at a new facility in Russia caused a 2-4 year delay in bringing an additional 30% of helium to market. The largest US helium production facility was also dealt a blow by fire, taking it partially offline until 2023.

The result of this instability has led the price of helium to spiral in the past few years. There is no public commodity market of Helium pricing therefore the pricing of helium is somewhat of a mystery when compared to openly traded hydrocarbon markets. Prices for crude helium (50%-60% concentration) at the BLM auction in 2018 were around ~$120/mcf. It is anticipated that the price for crude helium is currently trading at $500-600/mcf. High-grade helium with a +99% concentration commands a speculation price anywhere from $2000-$6000/mcf. These numbers are growing as the shortage continues and demand rises.

FINDING NEW SOURCES

Helium is a finite and non-renewable resource created terrestrially from the radioactive decay of uranium and thorium in the crust. The gas that doesn't escape to the atmosphere is trapped in conventional reservoirs commonly found with other natural gasses, including hydrogen and hydrocarbon gasses that make up most of our burning fuels.

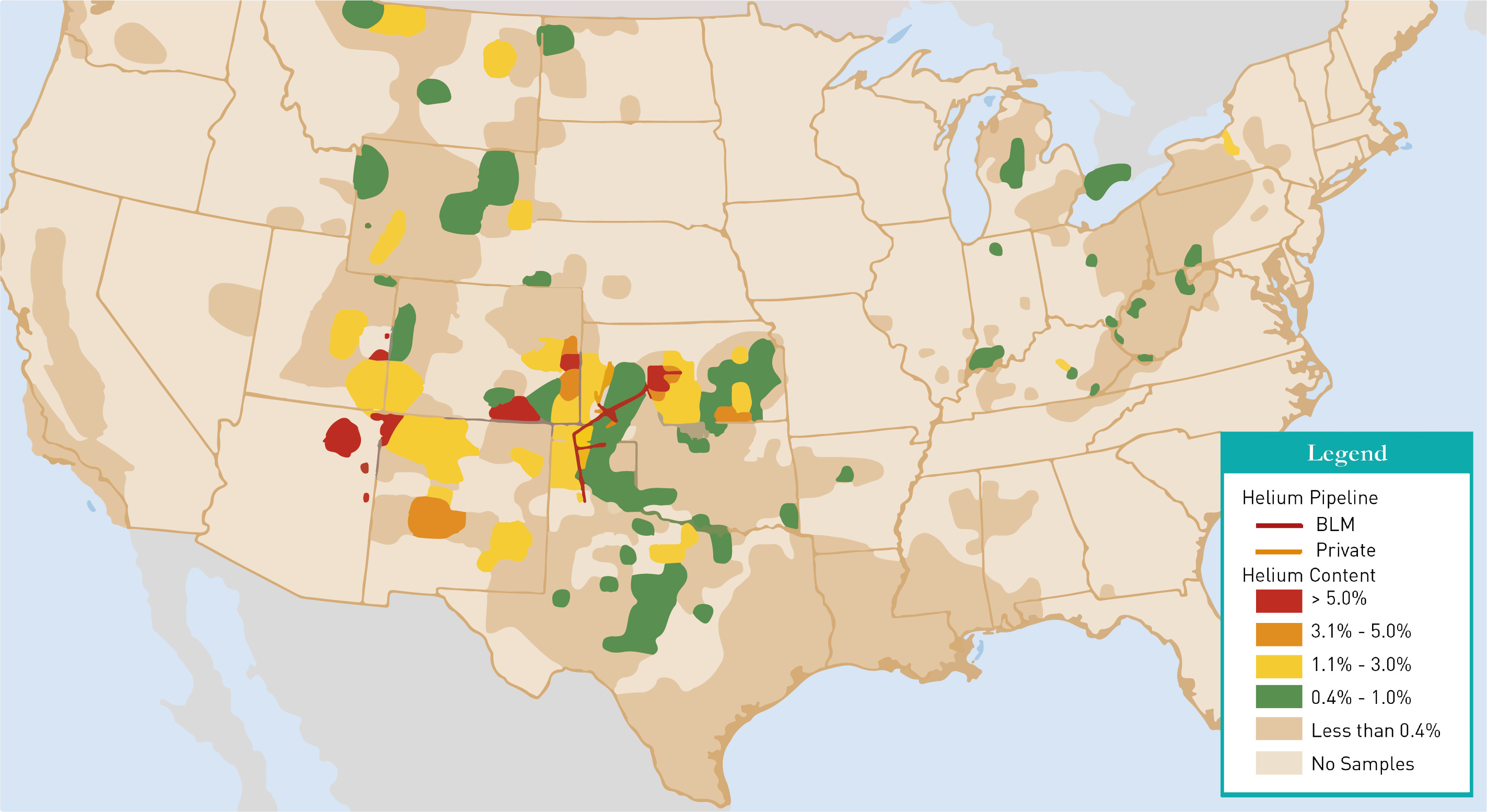

Algeria, Australia, Canada, Qatar, the US, and Russia are the largest helium producers. Historically, production was derived from extraction from natural gas processing, where less than 1% of the concentration was helium. However, in a few high-yield helium areas like the Texas Panhandle, Eastern Colorado, and NW Arizona, the concentration was over 3%. These fields are conventional reservoirs where anticlinal structures containing a Paleozoic age, porous sandstone, or Carbonates are overlain with a strong seal. In the US, unconventional shale exploration has driven hydrocarbon production for over a decade. Unfortunately, unconventional sources do not have high helium concentrations, and new discoveries have been rare.

FIGURE 1. Map of US helium resources

FIGURE 1. Map of US helium resources

As the demand and price of helium have risen, startups and existing supermajors have initiated new exploration to find more supply and develop new processing facilities near sources. A benefit of helium exploration is that reservoirs are conventional, and compared to modern unconventional horizontal shale exploration, the drilling process is generally straightforward. New wells are commonly vertical and tap into the apex of a contained trap. In addition, drilling vertically instead of horizontally expedites the engineering process and greatly reduces costs.

DATA EXPIDITES EXPLORATION

Finding significant helium accumulations is possible by examining historical well logs and well reports containing chemical analyses. Additionally, geologic knowledge of the basement-related structures helps assess the possibility of high concentrations of uranium and thorium-bearing granites and metamorphics. Companies like TGS have accumulated a vast database of historic well information, including exploration and production reports and Log ASCII Standard (LAS) files. TGS has also produced regional basin models using well and geologic data to map basement features.

Helium in large concentrations can be found in areas where hydrocarbon exploration was not profitable. Areas with ideal traps and reservoir structures but unsuitable hydrocarbon sources are feasible for helium and hydrogen storage. Arizona and Nevada are two examples of locations where structural traps are abundant. These areas have historical well data that is being used to find new helium reservoirs.

THE HUNT FOR HELIUM

The effects of the perfect storm around helium supply and demand will only grow more significant in the foreseeable future. Thankfully the oil and gas industry holds the extensive knowledge and experience needed to discover more of this elusive resource.

In the second Installment of the TGS Insight, we'll be looking at how modern subsurface imaging Is providing new Insight into the whereabouts of precious helium reserves.

With thanks to Jason Kegel (TGS) and Mark Germinario (Tumbleweed Midstream)